Vanishing Distinction: 403(b) Advisors Take on Other DC

Topics in 403(b) Distribution: first in a series

401(k) advisors troll the for-profit ponds while 403(b) advisors cast their lines into not-for-profit waters, right? Well, not exactly.

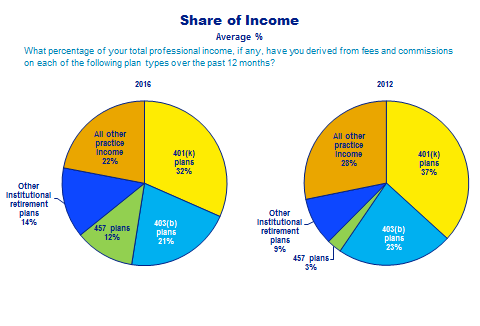

Updating our seminal 2012 study of advisors who sell 403(b) plans, we once again find that 403(b)-active advisors actually derive a significantly greater share of their income from 401(k) (32%) than from 403(b) (21%). Indeed, advisors’ share of income from 403(b) is virtually unchanged over the past four years, if anything drifting down slightly.

Up sharply over this period, however, is income associated with 457 and other institutional retirement plans, more than doubling from a combined 12% four years ago to 26% today. 401(k) and other practice income are down somewhat.

These and other findings from the new study reflect a growing focus on institutional business on the part of 403(b)-active advisors, three-quarters of whom now sell defined benefit or cash balance plans as well as non-qualified deferred compensation plans (57%) and cases of combined DC and DB plans (47%). The new 403(b) advisor is a very different breed from that of just a few years ago.

Exemplifying this shift is the Heavy 403(b) advisor which we define as those deriving 30% or more of their income from 403(b) (27% of 403(b) advisors). At 41%, their share of income attributable to 403(b) is almost double the 403(b) advisor average.

But it comes almost entirely at the expense of retail business; even these 403(b) specialists derive lots of income from 401(k) (31%) and 457 and other institutional retirement plans (22%).

About the Research

403(b) Advisors 2 was conducted in the fourth quarter of 2016 among 152 advisors deriving fee or commission income from non-proprietary 403(b) plans. Trend references are to an analogous Brightwork study conducted in the first quarter of 2012.