Emerging Market Focus: Sri Lanka

July 2016 | Insurance

By Yuen Leng Chin and Roshan Perera: Download

Yuen Leng Chin and Roshan Perera put Sri Lanka under the spotlight to highlight some of the innovations originating from the general insurance market and consider the future of disruptive development in light of the recent regulatory reform.

Emerging markets ‘leap frog’ in terms of evolution. They have a tendency for rapid development without the legacy issues or regulatory barriers that may inhibit growth and innovation as compared to more mature markets. As a result, emerging markets are often early adopters of technology and home to innovative product development and propositions. Mobile phone and internet users are omnipresent in these markets, largely driven by affordable products and services. Some of the offerings in the telecommunication space have caught up with, or even exceed, those of ‘mature’ markets. (It is common to find domestic broadband speeds of 1,000Mbps in South Korea, while a tenth of that speed is considered fast in much of the UK). There is also evidence of this type of progress in insurance markets in emerging and developing countries. Our focus for this article is Sri Lanka, a good example of a dynamic and vibrant insurance market which has embraced technology while undergoing significant regulatory reform.

A brief history…

Following the establishment of a state insurer in the early 1960s, the insurance industry in Sri Lanka was a virtual monopoly until the 1980s when the market was eventually liberalised. After liberalisation of the market in 1985, there were 15 composite insurance companies in operation by the turn of the century. Throughout this period of liberalisation, Sri Lanka was ravaged by a civil war which curtailed Foreign Direct Investment, resulting in most of the market expansion being led by domestic insurers, with very little exposure to international development. Up until 2010, over 60% of the market belonged to three of the 17 insurers operating at the time. The diagram below shows the Gross Written Premium growth rates of the UK and Sri Lankan markets over the period 2009 to 2015.

Surprisingly this insular oligopoly was the home to some of the most disruptive insurance propositions seen recently in Asia.

On-the-spot claims settlement

As with most countries in the region, the Motor class of business dominates most insurers’ portfolios, accounting for approximately 65% of Gross Written Premium. Following a detariffication of Motor and Fire rates in 2002 and 2005 respectively, the Motor insurance market entered a state of intense price competition. As with the evolution of the Motor market in the UK, the Motor insurance product in Sri Lanka became increasingly more commoditised with customers continuously seeking the lowest premium from insurers eager to capture market share. This market trend was the catalyst for a product innovation that shifted the focus of Motor insurance away from being a commodity product to a proposition based product.

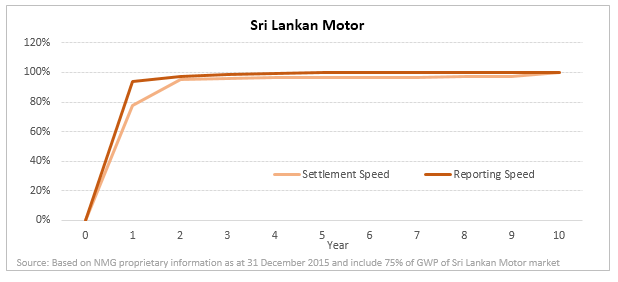

A private insurance company in Sri Lanka introduced the concept of ‘on-the-spot’ claims settlement for its Motor policyholders. The idea for the product was relatively simple. Customers who met with an accident would contact the insurance company, who would immediately dispatch a claims assessor to the scene of the accident to assess the damage and settle the claim on the spot, in full. Many Sri Lankan customers, who valued the certainty of an upfront claims settlement, switched to this company almost immediately, doubling its market share within the first two years of introduction from around 20% to 40%. The effect of this simple product innovation was profound in the Sri Lankan market resulting in a shift in focus to service; in this instance, the convenience and speed of the claim settlement, from price. Almost 10 years later, the company that introduced on-the-spot claims settlement continues to dominate the Motor insurance market, and is also able to charge higher average premiums than its competitors. This is impressive in a market where most companies competed purely on price. What’s more, the practice of fast claim settlement has become the industry norm (where the KPIs of the claims manager and loss adjustor are now based on hours and this has defined the payment patterns for Motor property damage in Sri Lanka). The diagram below shows the extreme short-tail nature of Motor business in the market, with over 90% of the claims being reported and almost 80% of the claims being paid in the first year.

To remain competitive in Sri Lanka, companies continued to innovate and leverage technological advances. The latest form of on-the-spot claims settlement involves a simple text message, notifying the claimant of their claim approval and availability of funds for withdrawal; a clever use of push notifications. Another company in the market recently developed the concept of ‘click-and-go’ where policyholders would take pictures of the damage using their smartphones and upload to the insurance company directly, eliminating the need for a claims assessor altogether.

Economic stabilisation and regulatory reform

These waves of innovations started during the civil war. At the time, Sri Lanka was in a high interest rate environment (ie. range from 10%-20%) which in turn led to a healthy investment income buffer for those companies able to attract premium income. As such, there was latitude for companies to experiment with pricing and propositions in a way that perhaps would not be possible in a tightly regulated low interest environment.

Following the end of the civil war in 2009, and a stabilisation of the economy, insurance companies were forced to revisit their strategies and move away from a top line only focus as underwriting results became more transparent. This also coincided with significant regulatory reform. In the past three years alone, the Sri Lankan insurance industry has dealt with a splitting of composite licenses, the introduction of a Risk Based Capital (‘RBC’) solvency framework, and a mandatory listing on the stock exchange. These developments have fundamentally changed the insurance landscape in Sri Lanka, where the regulatory changes and governance have led to a step change in technical capabilities throughout the market and with the implicit cross-subsidisation between Life Insurance and General Insurance now removed, insurers have had to reassess any underperforming businesses.

As the market has matured, we have also seen evidence of a change in the claims profile for the Motor insurance class with tails lengthening for the bodily injury component, possibly due to a better understanding of the cover, or an increased propensity to claim. As longer tails are associated with greater volatility, companies have expressed concerns on the expected claims and accompanying expenses that follow. Under the RBC regime, these higher reserves will also lead to higher capital requirements. The market leaders are now focussing on developing and strengthening competencies in an attempt to move beyond compliance and focus on technical underwriting in a soft market. The recently introduced RBC framework also requires any strategic decision to be supported by capital and any premium deficiencies to be identified.

Pushing the boundaries

While regulatory compliance has promoted a number of technical changes in the Sri Lankan insurance industry in recent years, resulting in a much more robust market, competition is still fierce and companies continue to seek a competitive advantage through product innovation. New propositions such as loyalty schemes and usage based insurance, using locally developed hardware and software, are currently under consideration.

With the increased availability of affordable technology and digitalisation, it is now possible to buy insurance using a smartphone or track driving behaviour via an application. Our experience is that emerging markets still appear to embrace innovation despite tighter regulatory frameworks. Competition will continue, requiring insurance companies to innovate to stay relevant. Successful insurers have been able to leverage technology and create significant first mover advantage despite rapid adoption by competitors of ideas that appear to work. These markets are also now relying on international best practices and new disruptive technologies to make improvements and create sustainable businesses.

Some may regard these innovations as gimmicks, others may see them as short-term fads, but maybe, just maybe, there is a thing or two the more mature markets could learn from their emerging market counterparts.

NMG has a strong affinity with the Sri Lankan market. As the largest supplier of General Insurance actuarial services in the market, NMG has contributed significantly to the uplift of technical competencies of the market in Sri Lanka, through our combination of skilled resources with Sri Lankan and international experience. To continue this conversation, contact Roshan Perera ([email protected]) or Yuen Leng Chin ([email protected]) at NMG Consulting.